Blog - 26/02/2019

Insurance Litigation

Can a landlord benefit from the Berni Inns Defence?

(Yes, but not even Fate can avoid the consequences of underinsurance)

The Berni Inns defence is the general principle that where one party (Party A) agrees to effect insurance for the benefit of itself and another (Party B), Party A implicitly agrees to exempt Party B from liability for causing an insured loss. In effect this means that Party A, and Party A’s subrogated insurer acting through him, cannot sue Party B for any such losses. This defence was established in Mark Rowlands Ltd v Berni Inns Ltd and Other [1985] WL 311082 (Court of Appeal) where Berni Inns Ltd, the basement floor tenant of Mark Rowlands Ltd, was protected from a subrogated claim by Mark Rowland’s insurers for the sums paid out to Mark Rowlands under the insurance policy.

It was clear in this case that the landlord had covenanted to insure the building against damage from fire and as the tenant had paid a separate insurance rent for this, they too were intended to benefit from the existence of the insurance policy.

The Berni Inns defence has since been applied in a variety of circumstances including, landlord and tenant cases, ship-owners and charterparties. These cases have examined the scope and application of the defence in great detail. In the recent case of Palliser Ltd v Fate Ltd & Others [2019] EWHC 43 (Palliser) it was considered for the first time whether a landlord, instead of a tenant, could benefit from the Berni Inns defence.

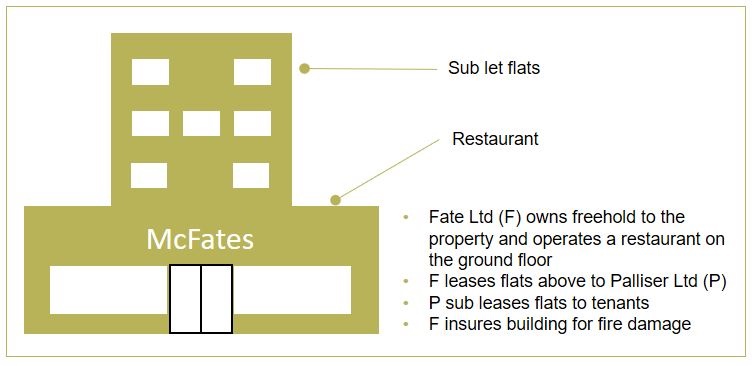

Facts of the case

Fate Ltd (F) owned and ran a restaurant on the ground floor of a property in London. F leased the upper three floors of this property, enclosing 7 flats, to Palliser Ltd (P) on a 999-year lease. P subsequently leased the 7 flats to various tenants. There was a fire in the ground floor restaurant on 1 January 2010, in which the restaurant was destroyed and the upper three floors extensively damaged.

P brought an action in negligence against F, which was settled in October 2017. In March 2018, P’s claim was allowed to continue under the Third Parties (Rights Against Insurers) Act 2010 against F’s insurers.

The Issue

Amongst other issues, the applicability of the Berni Inns defence in favour of F’s insurers was considered by the court. The question examined was whether P, under a 999-year lease, had impliedly excluded F’s liability in negligence, because F had agreed to purchase buildings insurance that covered fire damage to the building and any associated refurbishment costs. If the court found that liability in negligence had been excluded, then the claim under the Third Parties (Rights Against Insurers) Act 2010 would fail because F, although now insolvent, would never have been liable to P in the tort of negligence.

P submitted that the Berni Inns defence could not apply to this scenario because it was the landlord, rather than the tenant, who had been negligent. However, in the event that this argument failed, P submitted that the Berni Inns defence must be qualified in its application to the extent that F had underinsured the building.

Although Andrew Butcher QC, sitting as the High Court Judge, held that he did not need to answer the direct question of whether a landlord could benefit from the Berni Inns defence, he provided an analysis of the preceding case law and held that even if the defence did apply, it had to be qualified in its application. This was because the landlord had underinsured the building and a tenant cannot be said to have impliedly excluded a landlord’s liability in negligence, where the insurance provided by the landlord under the covenant to insure, was inadequate.

Although Andrew Butcher QC did not decide whether a landlord could benefit from the protection of the Berni Inns defence he did highlight its differences with the current case.

First, there was no subrogated claim in this case. Instead, it was a claim under the Third Parties (Rights Against Insurers) Act 2010 and therefore it was the landlord, and not the tenant, trying to invoke the defence.

Second, the question of financial contribution by the tenant to the insurance cover, a question which has been scrutinised in previous cases, was irrelevant here. It was the landlord in this case who was seeking to rely on an exclusion of liability and not the tenant.

Finally, the question of benefit under the insurance policy was clear, too. It was the landlord who had taken out the buildings insurance and therefore the landlord could undoubtedly benefit from the insurance to cover refurbishment costs incurred as a consequence of its own negligence.

Commentary

Palliser affirms previous case law by noting the relevant factors to be analysed when deciding whether the Berni Inns defence applies.

Palliser highlights the possibility that this defence can be quantified and applied in a limited fashion. It has created precedent that where a landlord has not complied completely with its covenant to insure the property, it will not be able to benefit fully from the Berni Inns defence.

If you wish to discuss this topic further or have any other questions, please contact Roger Franklin or any member of the Edwin Coe Insurance Litigation team.

If you aren’t receiving our legal updates directly to your mailbox, please sign up now

Please note that this blog is provided for general information only. It is not intended to amount to advice on which you should rely. You must obtain professional or specialist advice before taking, or refraining from, any action on the basis of the content of this blog.

Edwin Coe LLP is a Limited Liability Partnership, registered in England & Wales (No.OC326366). The Firm is authorised and regulated by the Solicitors Regulation Authority. A list of members of the LLP is available for inspection at our registered office address: 2 Stone Buildings, Lincoln’s Inn, London, WC2A 3TH. “Partner” denotes a member of the LLP or an employee or consultant with the equivalent standing.

Please also see a copy of our terms of use here in respect of our website which apply also to all of our blogs.